Sometimes, the hardest part of reviewing a company is seeing how much financial pressure it has gone through.

We recently evaluated a company with a history of losses and a significant amount of bank debt. Under normal circumstances, the repayment burden would have severely strained its cash flow.

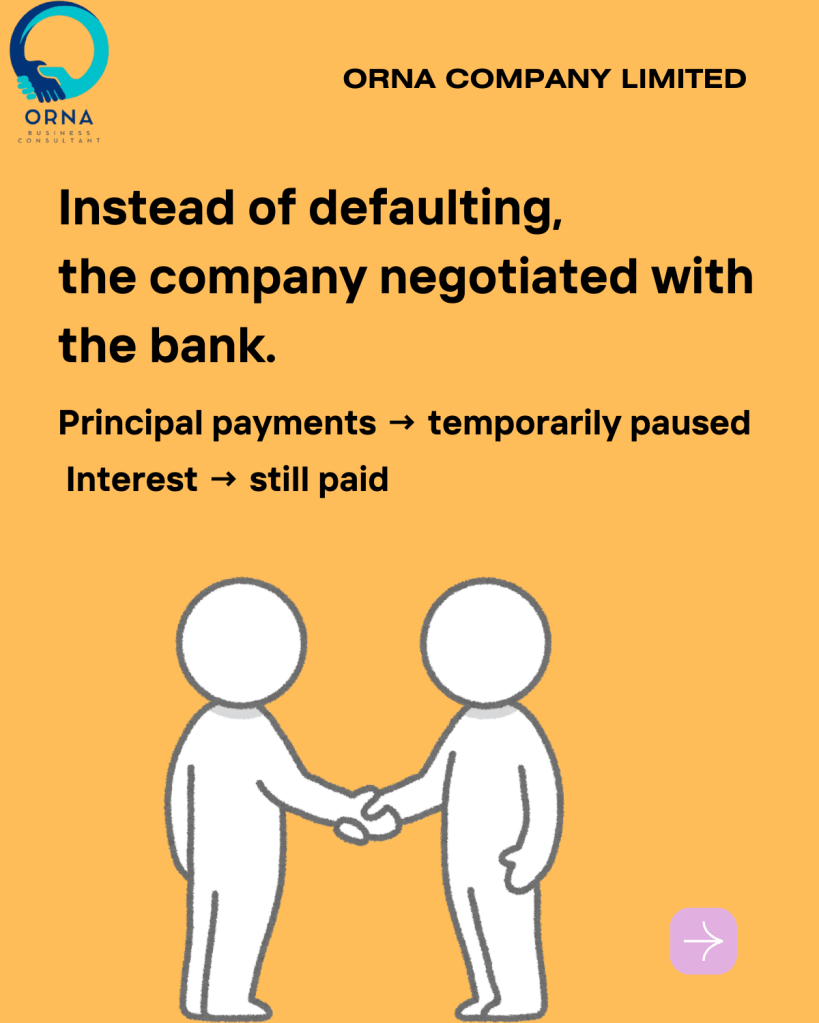

But instead of defaulting, the company negotiated with its financial institution to temporarily suspend principal repayment and service only the interest.

This decision made a critical difference.

It allowed the company to:

- preserve operating cash flow,

- continue running the business, and

- create time to recover performance.

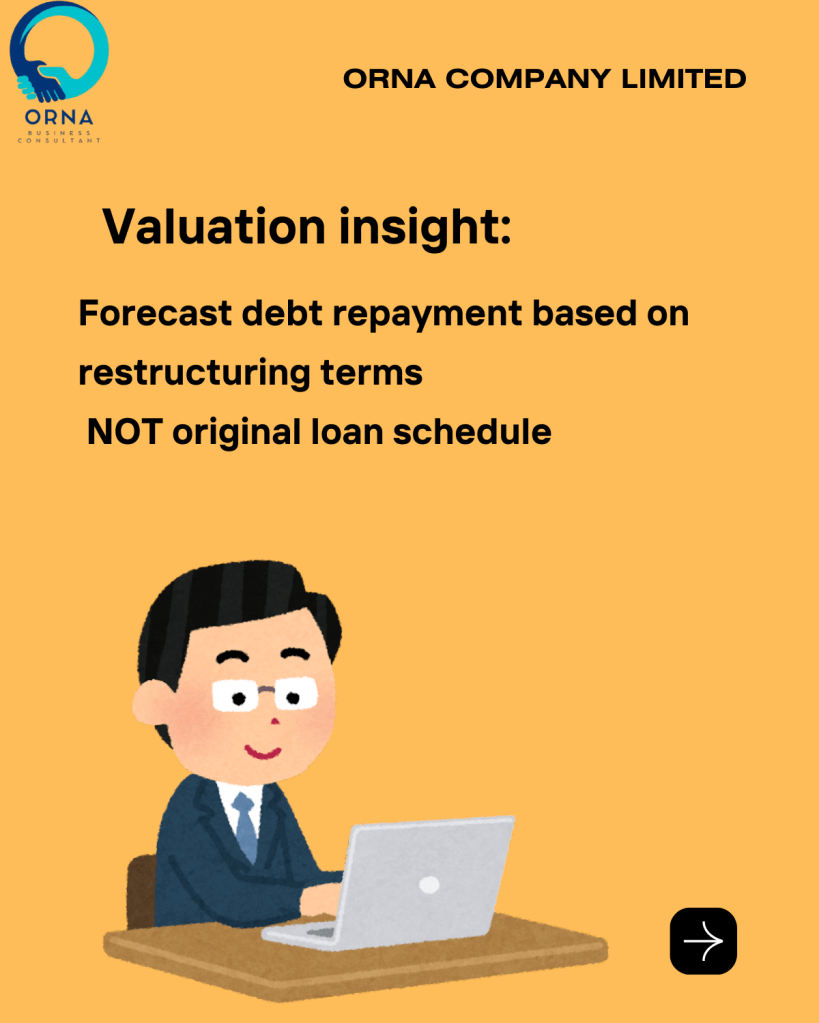

From a valuation perspective, this matters a lot.

When building our forecast model, loan repayments should not be based on original loan terms, but on the actual restructuring agreement. The revised repayment schedule showed that the company could realistically continue operations and potentially return to profitability — with the ability to repay debt in the future.

Debt restructuring may look alarming at first glance.

But sometimes, it is exactly what allows a business to survive long enough to recover.

Yes, the company is in trouble but it’s not the end of it yet and many very well recover.

#ORNA #Consult #DCF #Debt #BusinessValuation

Leave a comment